Dr. Nick Laskin

nicklaskin.ca

Partner with Dr. Nick Laskin. As the founder of Fractional Quantum Mechanics (FQM), Nick brings foundational physics to quantitative finance to solve the markets where standard math breaks.

The fractional Schrödinger equation governs the probabilities of sudden, non-local quantum jumps.

Traditional risk models like Black-Scholes rely on a fatal flaw: they assume that market prices follow continuous, smooth paths with constant volatility ($\sigma$) and zero memory.

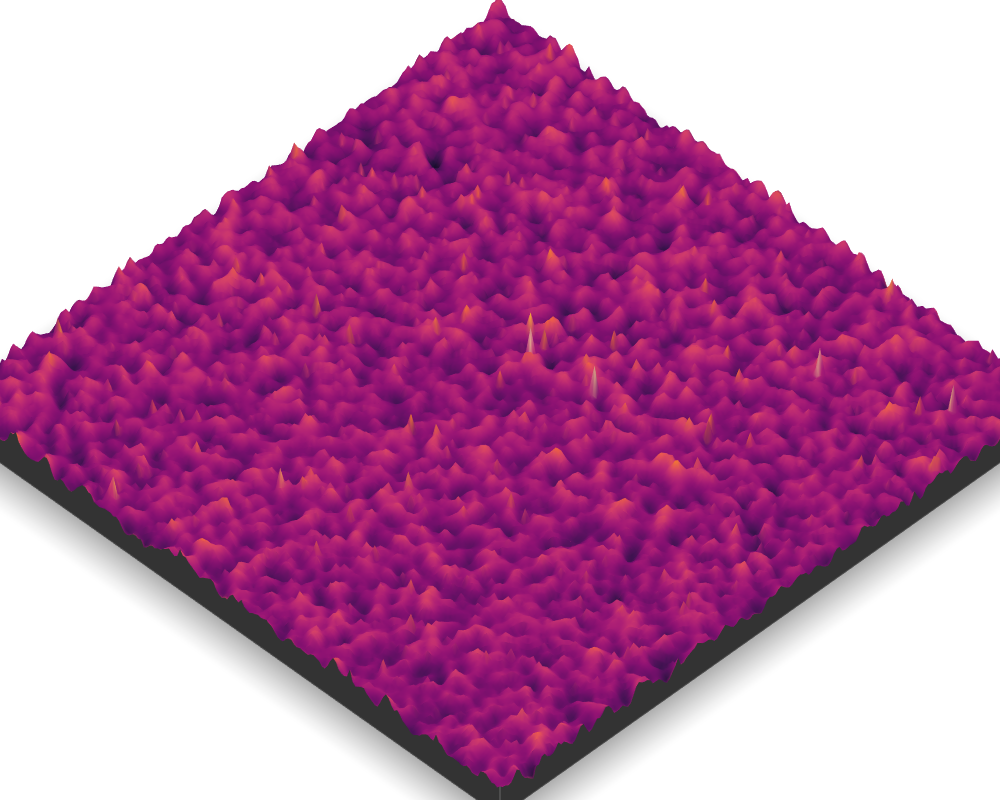

Standard models ignore the jumps that traders actually live through. The pervasive Volatility Smile proves that real-world markets experience violent jumps, sudden shocks, and structural memory.

Relying on memoryless continuous-diffusion models leads to underpriced tail risk and suboptimal algorithmic execution.

Dr. Laskin's Geometric Shot Noise (GSN) and fractional stochastic models see the structural dependencies that memoryless models miss. By incorporating long-range memory and correlated jump-diffusion directly into the pricing kernel, we give hedge funds and risk managers the tools to price real-world risks accurately and capture alpha.

Continuous, smooth paths. Volatility is assumed constant. Zero memory of past shocks.

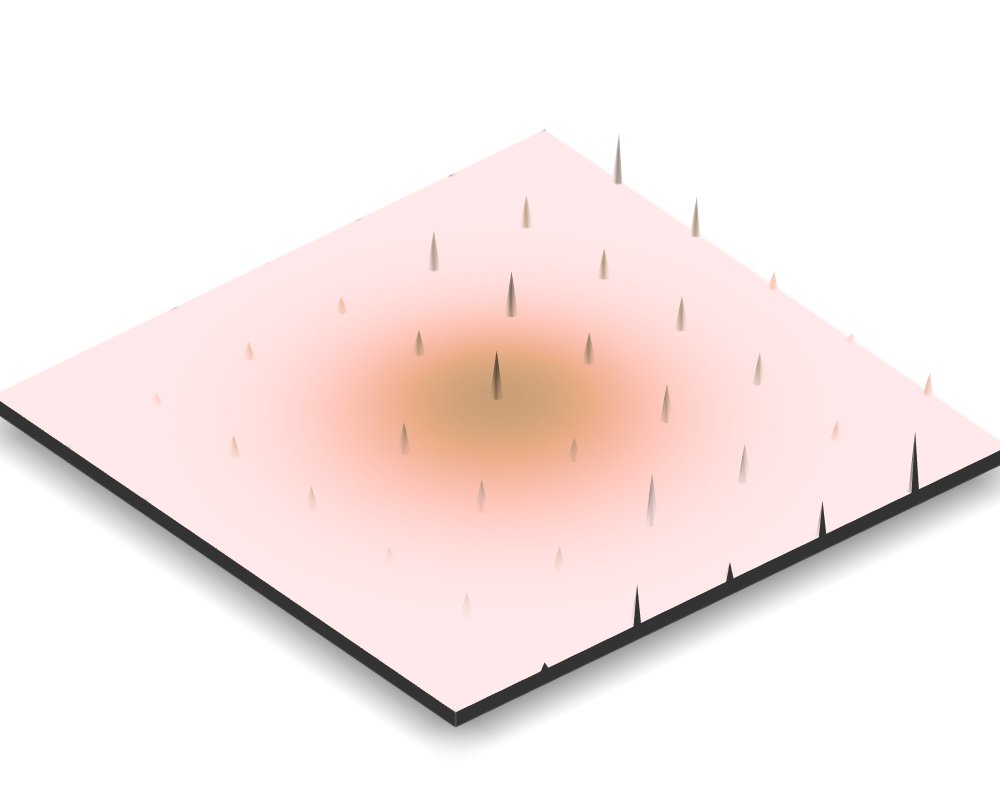

Discontinuous jumps with fractional waiting times. Past events cluster and decay slowly over time.

Dr. Laskin bridges foundational quantum physics and high-performance financial engineering. While black-box AI models fail to predict structural shocks because they merely extrapolate past trends, foundational physics models the underlying generative processes of market jumps.

Research Scientist | Ukraine

Collaborated with physics legends A.I. Akhiezer and S.V. Peletminskii. Focused on quark-gluon plasma instabilities, dense neutron matter magnetohydrodynamics, and predicted coherent Bremsstrahlung suppression in oriented crystals.

Department of Electrical & Computer Engineering | Canada

Founded Fractional Quantum Mechanics (FQM), generalizing Feynman path integrals over Brownian paths to Lévy flight trajectories. Discovered the Fractional Schrödinger Equation.

Department of Systems & Computer Engineering | Canada

Formulated the Riemann-Liouville Fractional Lévy Motion (fLm) and Fractional Poisson Process (FPP), introducing heavy-tailed $\alpha$-stable noise and Mittag-Leffler waiting times to model non-Markovian network traffic and self-similar data queueing.

Visiting Scholar | New York, USA

Applied fractional dynamics and Lévy flights to financial engineering, analyzing log-moneyness, the volatility smile, and econophysics modeling.

Principal Consultant | Canada

Providing bespoke consulting services in quantitative finance algorithm development, stochastic systems auditing, and complex systems architecture.

This mathematical framework fixed how we calculate tail risk and structural dependencies across industries by introducing fractional waiting times and long-range memory.

Standard Black-Scholes approaches are replaced with Geometric Shot Noise (GSN) models. These models properly capture volatility clustering and memory-driven market shocks, accurately reflecting the true nature of risk.

The Fractional Poisson Process predicts bursty packet traffic and mitigates server bottlenecks, solving queueing systems for high-frequency trading networks and telecommunications.

Robust mathematical models capture real-world fractal timing by identifying structural dependencies. This replaces flawed first-order Markovian models with fractional-order memory systems.

Fractional Quantum Mechanics and Disorder Engineering predict atomic-level material defects, creating high-fidelity models for semiconductor growth.

An intuitive breakdown of Dr. Laskin's work: why classical math fails when systems jump, and 4 practical applications across finance, router RAM, semiconductors, and quantum computing.

Read Layman's Guide →

Discover how tuning Laskin's Riesz derivative ($\alpha$) continuously morphs quantum statistics from Bosons to Parafermions to Fermions, with applications in structured light photonic quantum gates.

Read Deep Dive →

Explore Dr. Laskin's 2000–2002 Carleton invention: an alternative to Kolmogorov-Mandelbrot fBm and a Generalized Router Buffer Model predicting heavy-tailed packet loss.

Read Deep Dive →Experience the power of fractional dynamics. Adjust the sliders to contrast the violence of the Lévy Flight against the passivity of Brownian motion, revealing the hidden geometry of financial markets and complex systems.

Solve the transcendental equations for InGaN/GaN wells. Adjust the Lévy Index $\alpha$ to model impurity-induced disorder (Brownian limit is $\alpha = 2.0$).

Target a transition emission wavelength:

Simulate event counts $N(t)$ driven by Mittag-Leffler waiting times. Notice the "bursty" behavior and long flat gaps (memory trapping) as $\mu$ decreases below 1.0.

Calibrate the Geometric Shot Noise process. Increase jump frequency or magnitude to see the volatility skew/smile emerge from the underlying shot-noise shocks.

Dr. Laskin's published monographs establish FQM and FPP as recognized academic sub-disciplines, bridging theoretical physics with real-world applications. These defining works compile decades of research into comprehensive guides for academics and industry professionals alike.

World Scientific Publishing

The definitive text on FQM. Covers paths integrals over Lévy flights, fractional uncertainty relations, analytically solvable wells, fractional Bohr atoms, and time-fractional non-Markovian dynamics.

World Scientific Publishing

The first dedicated book on FPP. Systematically details the Kolmogorov-Feller fractional equations, renewal theory, inverse stable subordinators, and direct Mittag-Leffler probability design, with multi-disciplinary applications.

Quantitative Modeling & Semiconductor Consulting

Dr. Laskin offers specialized consulting engagements for institutions seeking to integrate fractional quantum mechanics into their proprietary risk models or material simulations. Through targeted advisory, organizations can leverage non-local mathematical frameworks to solve complex volatility pricing and manufacturing yield challenges.